Think Your Home Insurance Payout Is Short? Here’s How to Challenge It with Confidence

If your insurance check feels smaller than the damage you see, you’re not alone. After storms, fires, leaks, or other losses, many homeowners receive estimates that miss critical line items, underprice labor, or overlook building code requirements. The good news: you can challenge an underpaid claim using clear documentation, practical steps, and a calm, organized approach. This article walks you through how to spot shortfalls, gather the right evidence, and request a fair supplement from your insurer—without turning the process into a full-time job.

Why Homeowners Often Get Shortpaid

Insurers rely on adjusters and estimating software to price your repairs, but those estimates aren’t perfect. Common causes of low payouts include:

- Scope gaps: Missing rooms, elevations, or related components (for example, painting only one wall when the whole room is affected).

- Omitted line items: Missing roof accessories, drip edge, starter/cap shingles, ice/water shield, underlayment, ridge vents, kickout flashing, window wraps, or baseboards.

- Outdated or non-local pricing: Labor and material rates that don’t match your current market.

- Code upgrades: Required items under local building codes (arc-fault breakers, nail patterns, underlayment types, ventilation) not included.

- Overhead and profit (O&P): Not included on complex jobs that need multiple trades or a general contractor.

- Waste and haul-off: Insufficient waste factors for roofing, flooring, or siding, and missing dump fees.

- Taxes and permits: Sales tax, permit fees, and inspection costs left out.

- Matching and continuity: Repairs that won’t match undamaged areas, resulting in an inconsistent finish.

- Moisture and mold remediation: Drying, dehumidification, HEPA filtration, containment, and testing not fully captured.

Spotting these issues early helps you make a strong, well-documented case for a corrected estimate and appropriate payment.

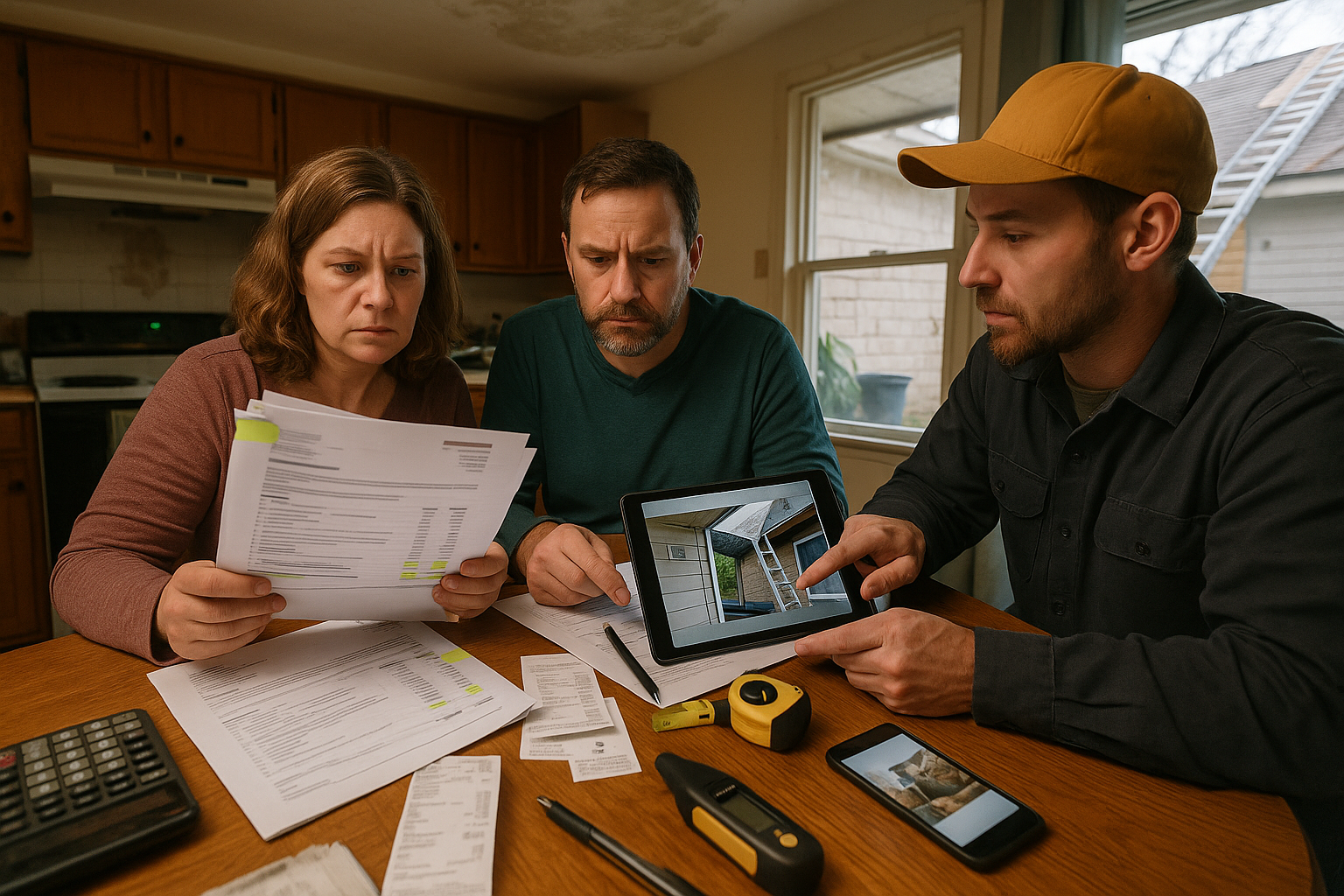

Audit Your Estimate Step-by-Step

You don’t need to be a contractor to perform an initial review. Use this quick process to identify gaps:

- Gather everything: The insurer’s estimate, photos, your policy declarations, endorsements, any contractor bids, code citations, permits, and receipts for emergency repairs.

- Match scope to visible damage: Walk each affected area with the estimate. Check if the listed line items fully address the actual damage you see.

- Check the structure of the estimate: Look for missing trades (electrical, HVAC, drywall/texture, paint, insulation, roofing accessories), clean-up, and protection of property.

- Review unit costs: Compare line-item pricing to current local rates. If a contractor’s written bid is higher, note the differences in scope and unit costs.

- Confirm code compliance: Ask your city or county building department website for applicable code requirements for your repair. Save links or PDFs.

- Depreciation math: If you have replacement cost value (RCV) coverage, the first check may be actual cash value (ACV). Note what’s being held back and what documentation is needed to recover the withheld depreciation.

- O&P eligibility: If your repair requires multiple trades and coordination, document why a general contractor is needed and add customary O&P.

- Photos and labeling: Take clear, well-lit photos. Label them by room/elevation and tie each to a line item or missing item.

- Time-sensitive items: Keep logs of additional living expenses (ALE), temporary repairs, and mitigation invoices.

For a deeper walkthrough of the dispute process, see this helpful insurance claim dispute resource: Insurance Claim Dispute Guide.

Evidence That Strengthens Your Request

Your goal is to present a factual package that makes it easy for the adjuster to say yes. The strongest evidence includes:

- Comparable contractor estimates with detailed line items and current local pricing.

- Manufacturer specifications showing required installation or materials (for example, required underlayments or fasteners for your roof type).

- Printed or linked local code citations that necessitate certain upgrades or methods.

- Photos with annotations pointing to each missing or underpriced item.

- Moisture maps, drying logs, and remediation protocols for water losses.

- Weather verification reports for storm dates, if relevant.

- Permits, inspection notes, or city guidance related to your repair plan.

Organize these in a single PDF or shared folder with a short index. Clarity and organization often determine how quickly a supplement gets approved.

How to Ask the Insurer for a Supplemental Payment

Once you’ve identified gaps and gathered documentation, submit a concise request:

- Subject line: Include your claim number and the word “Supplement.”

- Summary first: In a brief paragraph, explain what’s missing or underpaid and the total amount requested.

- Attach evidence: Contractor estimate, code references, photos, receipts, and any permits.

- Explain O&P and complexity: If multiple trades are involved, note why a general contractor is required and the customary O&P percentage in your market.

- Request reinspection if needed: Ask for a joint site visit with your contractor or estimator.

- Ask for a written response: Request a written explanation for any line items they decline to fund.

Be professional and factual. Keep a claim diary with dates, who you spoke with, and what was said. If the adjuster changes, forward your summary and evidence so the new handler can get up to speed quickly.

Appraisal, Reinspection, and When to Bring in Help

If you’re at an impasse, you may have options within your policy to move things forward:

- Reinspection: A second look with new evidence, ideally with your contractor present to discuss scope and methods.

- Appraisal clause: Many policies include a process where each side selects an appraiser, and an agreed umpire resolves pricing and scope differences. Check your policy for details and timelines.

- Third-party support: Licensed contractors, independent estimators, or public adjusters can help document scope and pricing. Choose experienced professionals who understand local codes and insurer estimating platforms.

Always review your policy conditions and deadlines before initiating any option. Keep communications focused on facts, documentation, and your goal: restoring your home correctly and safely.

Timing, Deadlines, and Common Pitfalls

Disputes move faster when you stay ahead of the process. Watch out for:

- Missing policy timelines: Proof-of-loss requirements, appraisal request windows, and other conditions can be time-sensitive.

- Partial documentation: Submitting a supplement without clear evidence often leads to delays or denials.

- Untracked ALE: Save receipts and keep a simple spreadsheet for additional living expenses if you’re displaced.

- Mortgage company endorsements: If your check lists a mortgagee, contact the lender early to ask about their endorsement process and inspections.

- Starting work without alignment: If possible, get written agreement on scope and pricing to avoid surprises mid-project.

- Not recovering depreciation: For RCV policies, submit completion documentation promptly to release withheld depreciation.

FAQ

- What is a “supplement” to an insurance claim?

A supplement is a request to adjust the original estimate when new damage is discovered or when pricing, code items, or scope were missed. It’s common and often necessary for complex repairs.

- Will disputing my claim increase my premium?

Premium changes depend on many factors, including carrier practices and the type of loss. Asking for accurate payment on a covered claim is a normal part of the process. Your insurer can explain how claims history affects rates.

- How long does a supplement take?

It varies by carrier and complexity. Well-organized requests with clear evidence typically move faster. Expect anywhere from a few days to several weeks, especially if reinspection or appraisal is involved.

- What if I already deposited the check?

Depositing the initial payment doesn’t usually close the claim. If your policy provides replacement cost coverage, you can often seek additional funds through supplements or depreciation recovery with proper documentation.

- What’s the difference between ACV and RCV?

ACV (actual cash value) is the depreciated amount; RCV (replacement cost value) is what it costs to restore with new materials. With RCV coverage, you may receive ACV first, then the balance after repairs and documentation.

- Do I need a contractor’s estimate to dispute the claim?

It’s not always required, but a detailed, locally priced contractor estimate is one of the most persuasive pieces of evidence you can provide.

A Smart, Practical Path to a Fair Outcome

You don’t have to accept an estimate that doesn’t truly restore your home. By methodically reviewing the scope, gathering strong evidence, and communicating clearly, you can often secure a corrected estimate and the funds necessary to complete the job safely and to code. If you want quick feedback on where your estimate might be light—and what to do next—use our simple review tool to get started: Check my claim.